Back to Projects

Monte Carlo Simulation Options Pricing

PythonFlaskReactTypeScriptyFinance

About

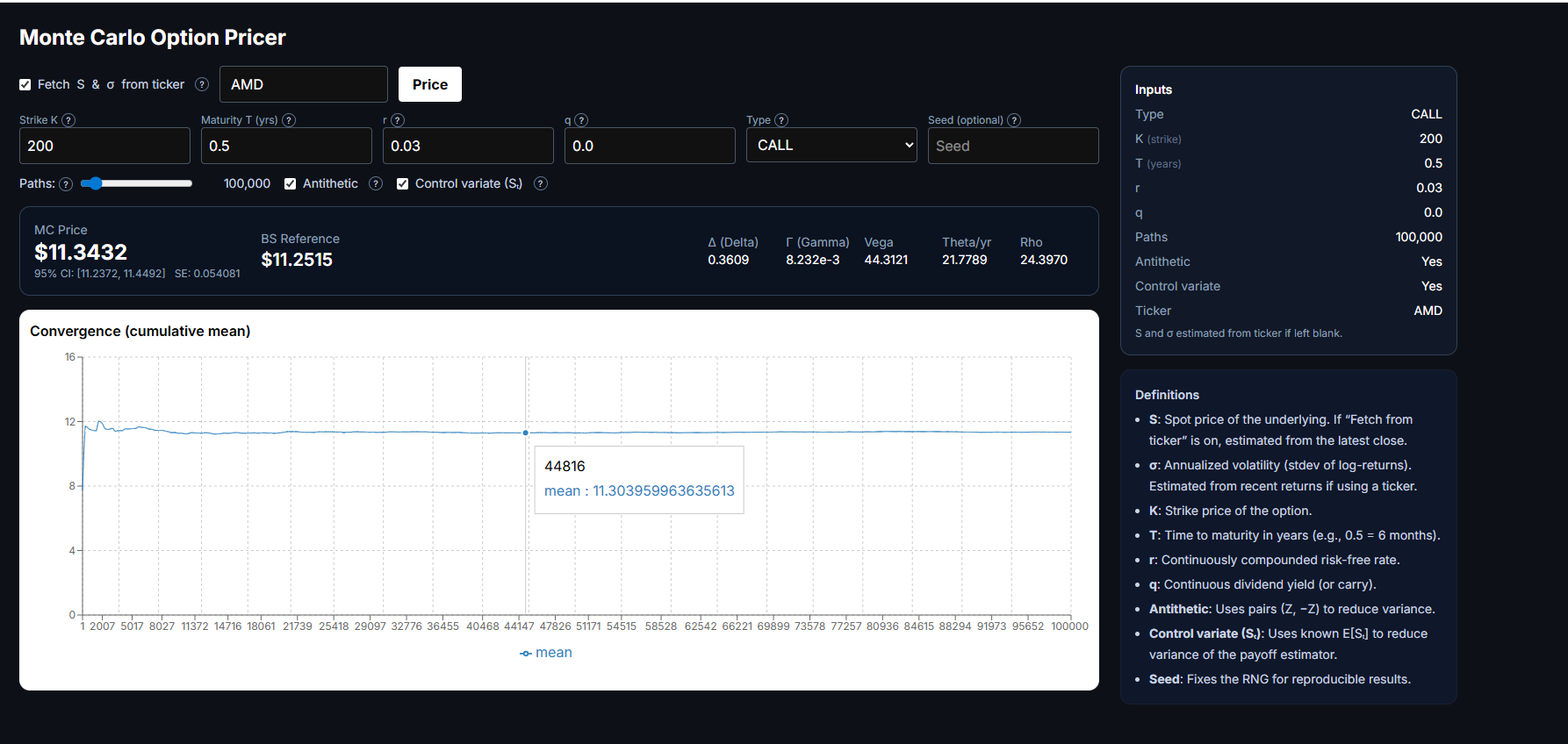

An interactive option pricer that estimates fair values and Greeks by simulating the terminal stock price under geometric Brownian motion. The app can pull the spot price and a realized annualized volatility directly from a ticker (via recent returns) or accept manual inputs, then runs a variance-reduced Monte Carlo with antithetic pairs and an optional control variate on S_T for tight confidence intervals. Results include the MC price, 95% CI, standard error, and a convergence plot of the cumulative mean to show numerical stability. For validation, a Black–Scholes reference is computed with the same inputs, and Greeks (Delta, Gamma, Vega, Theta, Rho) are obtained by bump-and-revalue using the same RNG stream so they’re consistent and low-noise. A seed parameter provides reproducible simulations, while practical defaults (e.g., 100k paths, antithetic on, control variate on) ensure accuracy without guesswork.

Gallery